Introduction

In July 2024, the Government of India introduced Form GSTR-1A, a significant amendment under the Goods and Services Tax (GST) regime. This optional form allows taxpayers to correct or add details to their previously filed GSTR-1, ensuring that their returns are accurate before the final submission of GSTR-3B. This will guide you through the essential aspects of Form GSTR-1A, its purpose, and how to utilize it effectively.

What is Form GSTR-1A?

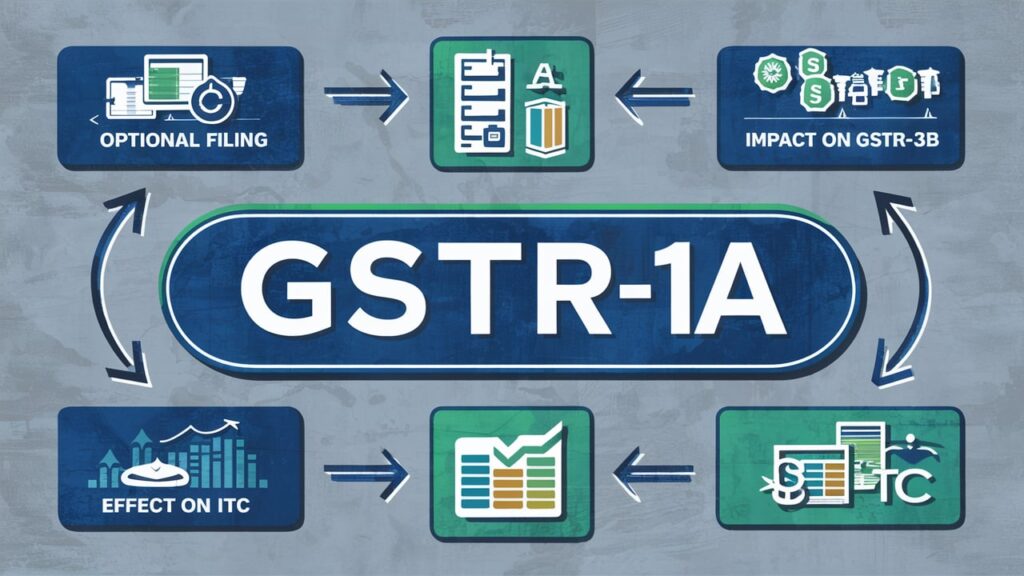

Form GSTR-1A is an optional facility introduced via Notification No. 12/2024 – Central Tax, dated July 10, 2024. It allows taxpayers to amend or add details of outward supplies for the current tax period, which may have been omitted or wrongly reported in the GSTR-1 filing. This return is essential as it provides taxpayers with an opportunity to rectify their records before the finalization of GSTR-3B of the said tax period, ensuring that the invoices for outward supplies reported is accurate and up-to-date.

Key Features of Form GSTR-1A

- Optional Facility: Form GSTR-1A is optional and can be filed only once for a particular tax period. This makes it important return for those who wish to correct or update their filed GSTR-1 for the said tax period.

- Impact on GSTR-3B: Any changes made through Form GSTR-1A will reflect in the corresponding GSTR-3B of the same tax period. This ensures that the taxpayer’s liabilities are accurately reported.

- Recipient’s Input Tax Credit (ITC): The amendments made in GSTR-1A will affect the ITC of the recipient for the next tax period, as these changes will be visible in GSTR-2B.

- Availability:

- For monthly filers, Form GSTR-1A will be available from the due date of filing GSTR-1 or the actual date of filing, whichever is later, and will remain open until the actual filing of GSTR-3B

- For quarterly filers, Form GSTR-1A will be available from the due date of filing GSTR-1 or the actual filing date, whichever is later, and will remain open until the GSTR-3B filing for that quarter.

When Should You File Form GSTR-1A?

Form GSTR-1A is available from the later of two dates: the due date of filing GSTR-1 or the actual filing date of GSTR-1. The form remains open until the actual filing of GSTR-3B for the same tax period. It’s essential to note that once GSTR-3B is filed, GSTR-1A cannot be used for that tax period. For filing of GSTR -1A , visit this website.

Is It Mandatory to File Form GSTR-1A?

No, filing Form GSTR-1A is not mandatory. It is an optional form, primarily used for correcting or adding details to GSTR-1. Taxpayers should consider using it if they need to amend any supply records before the final submission of GSTR-3B.

Common Scenarios for Filing Form GSTR-1A

Adding Missed Records: If a taxpayer missed adding any records while filing GSTR-1, they can use GSTR-1A to include those records.

Amending Incorrect Records: If any records were incorrectly reported in GSTR-1, the taxpayer could use GSTR-1A to correct these mistakes before finalizing GSTR-3B.

Limitations of Form GSTR-1A

Cannot File Nil GSTR-1A: If there are no amendments or additions to be made, the taxpayer cannot file a nil GSTR-1A.

Single Use per Tax Period: Form GSTR-1A can only be filed once for a particular tax period, even if GSTR-3B is not filed.

Want to learn about Income Tax Return filing in detail? Check out this Post

FAQs

1. Who can file Form GSTR-1A?

– Example: If GSTR-1 for August 2024 is furnished on September 10, 2024, and the taxpayer realizes a mistake in two records while also missing one record, GSTR-1A will be available from September 10 or the due date (September 11), whichever is later. The taxpayer can amend the incorrect records and add the missed record in GSTR-1A, which will be auto-populated in GSTR-3B.

2. When is GSTR-1A available for filing?

1. Due date of filing GSTR-1 (11th of the following month).

2. Actual date of filing GSTR-1.

– For quarterly filers, it’s available from the later of the following two dates until the filing of GSTR-3B for that quarter:

1. Due date of filing GSTR-1 (13th of the month following the end of the quarter).

2. Actual date of filing GSTR-1 (Quarterly).

3. What is the due date for filing Form GSTR-1A?

4. Can I file Form GSTR-1A after filing Form GSTR-3B?

5. Is it compulsory to file Form GSTR-1A?

– To add new records missed during GSTR-1 filing.

– To amend records already reported in the same period’s GSTR-1.